Facebook Shops, Amazon, and the Future of Ecommerce in America

by Tom Humphrey and Willa Sobel

State of Play

The demands of digitally-reliant consumers and a post COVID-19 world are ensuring that the ecommerce industry is gearing up for major disruption in the coming years.

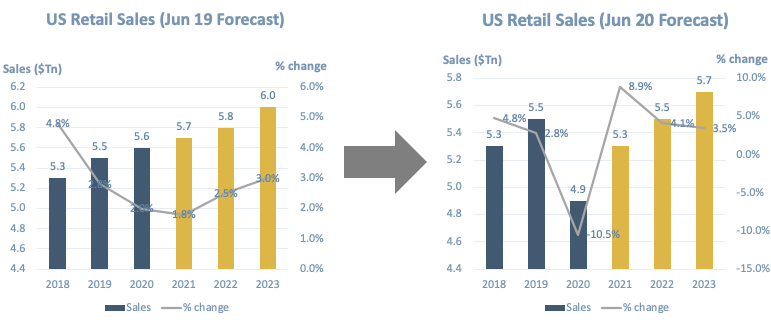

Before exploring where we are heading, it is important to understand where we are. In 2019, total retail sales topped $25 trillion globally growing steadily around 4% each year the past half decade. Of this, the US accounted for $5.5 trillion which was (pre-covid) expected to grow by 2.8% to $5.6 trillion in 2020. COVID has naturally thrown a wrench into the mix. Due to the pandemic’s significant demand shock, store closures, and stay-at-home orders, total US retail spending is now expected to decline around 10.5% to $4.9 trillion in 2020.

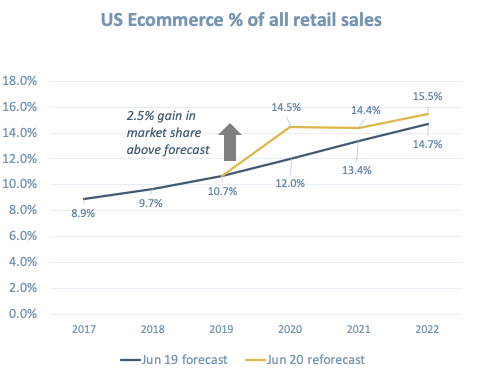

Ecommerce has gradually been chipping away as a share of total retail sales over the years, increasing from 8.9% of all sales in 2017 ($450 billion) to 11% in 2019 ($601 billion). If one were to focus solely on the sale of “general merchandise”, 2019 was actually a milestone year with total online sales exceeding physical sales for the first year ever. COVID has also had the impact of speeding up the transition to online sales, and in 2020 approximately 14.5% of all goods sold in the US are expected to be web-transacted, an alltime high, the biggest share increase of any year and a 2.5% gain in market share of sales above original pre-COVID forecasts.

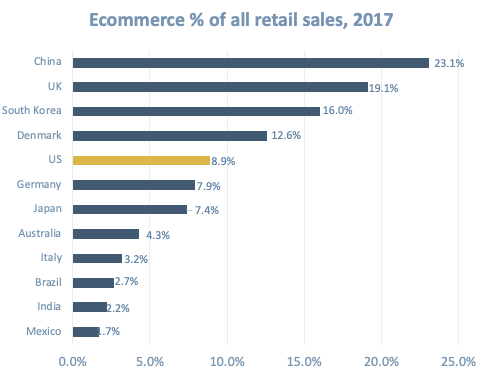

That said, and despite the growth of Amazon, the US is well behind other countries, most notably China. In 2017, while 9% of retail sales in the US was conducted online, China saw 23%, the UK at 19% and South Korea at 16%. India is well behind at 2.2%, which combined with a 1.4 billion population is perhaps why everyone is jumping in so aggressively on Jio.

China has seen huge innovation in the ecommerce space over the past decade with JD.com, Alibaba, Tencent, and Pinduoduo (the company that you’ve never heard of that is actually listed on the NASDAQ and is the fastest company ever to hit a US $100B valuation, reaching that achievement less than 5 years after its founding). So obviously a lot of room for continued growth.

In 2017, ecommerce accounted for 23% of all retail sales in China versus only 9% in the US

Given the shift to ecommerce was already well underway, the effects for physical retail are likely to be lasting. How things shake out from here with covid is uncertain and largely depends on the course of the pandemic, regulatory responses in terms of stay at home orders and retail restrictions, and new technologies to enable safe shopping. In the short term, luxury and discretionary purchases or those related to travel and outdoor activities will continue to be hurt more than purchases of necessity such as groceries and purchases for home use and entertainment. Even french luxury conglomerate LVMH shifted normal supply chain operations to produce hand sanitizer during global shortages. Supply chains (production, manufacturing and shipping) will continue to be severely disrupted.

Beyond the shift to ecommerce, another big theme has been consolidation. Amazon, Walmart, and Shopify are industry powerhouses and continue to rapidly innovate to compete and grow. Much of the ecommerce market today is directly attributable to Amazon, which is growing at above-market rates and is expected to account for 38% of all online sales in 2020. No doubt the desire for reliable delivery, improving turnarounds of click-and-collect fulfillment, and the expansion of goods offered into groceries and other lines is driving this. The top 10 online retailers in the US now have approximately 60% market share. Although, with recent moves by congress and administration to break up big tech, Amazon may well be laying low for a while.

———————-

Key Themes

A couple of key technology trends are looking to define the ecommerce industry moving forward:

1/ Mobile purchasing will continue to grow through technology enhancements such as Augmented Reality (AR).

Mobile sales have increased as a share of US ecommerce sales from 34.5% in 2017 to 49.2% in 2020. Yet despite this, conversion rates on mobile are less than half than on desktop. Many companies are shifting to be “mobile first” in their approach with new technologies such as accelerated mobile pages and progressive web apps affording improved shopping opportunities and faster loading.

Recent enhancements in AR are breaking down one of the biggest barriers to e- purchasing today — the inability to “try things on”. This factor, combined with the promise of “free returns”, means that consumers often make erroneous purchases, leading to significantly higher return rates. Approximately 8–10% of instore purchases are returned compared to over 20% for ecommerce, driving a significant cost line for online retailers. By affording consumers the ability to visualize their purchases in their home or on their bodies, AR will increasingly close that gap. For example, Warby Parker and Sunki now allows consumers to try on glasses virtually online pre-purchase (overlaying the glasses to your computer’s video). Threekit and Seekxr are two examples of companies spearheading the AR initiative for other ecommerce companies.

2/ The rise of vCommerce (or voice powered commerce) and digital voice assistants.

There are expected to be 8 billion digital voice assistant enabled devices in the market by 2023, and the smart speaker market is projected to hit $36 billion by 2025 (up from $12 billion in 2019). VCommerce conversational chatbots are rapidly improving and increasing their share of retail sales, yet have not taken off as fast as was initially expected, largely due to consumer concerns over privacy and the need for enhancements to overcome errors (some quite funny!). The rise of vCommerce is also expected to have a major impact on SEO as the focus switches to emphasize optimization for voice over search results.

3/ Artificial Intelligence and automation will streamline workflows and enhance personalization.

Personalization in online retail is nothing new — already by 2014, upwards of 73% of retailers offered some form of basic website personalization leveraging location data and curating a targeted consumer experience, but strategies are rapidly getting more sophisticated. Perhaps no company encapsulates the opportunity for the use of data, AI, and personalization in the retail process more than Stitch Fix, the personal styling company that curates and ships personalized outfits based on mass data analysis of preferences and behaviors. Some areas where AI and automation is enhancing the ecommerce value chain include:

- Product merchandising — supporting relevant product assortment and “customer-centric search” to improve conversions, automatically preloading storefronts for major events, real-time pricing adjustments and “flash sales”

- Marketing — optimizing messaging and channel mix and automating the engagement of customers based on known profile and behavior, streamlining tracking and reporting

- Inventory — automating inventory alerts and the scheduling of reordering, analyzing sales to identify product development opportunities, warehouse robotics

- Support — assisting customers with their questions instantaneously to improve NPS and reduce support costs (as much as 85% of interactions will be moderated without human presence in 2020)

- Fraud — identifying and flagging / cancelling high-risk orders (e.g. NS8 in Nevada recently raised a $123m series C to reduce fraud through behavioral analytics)

4/ Brands will grow their Direct-to-Consumer channel and transition to social media platforms for retailing.

A number of factors have been driving major brands to look to grow their direct to consumer sales channels — 1) the growing threat of retailer private labels (now expected to account for almost 20% of all consumable sales), 2) the shift to ecommerce and mobile sales (in 2015, it was reported that 70% of shoppers made mobile purchases, which has only grown since), 3) the desire to own the customer relationships and data, 4) the proven success of DTC companies such as Dollar Shave Club and Warby Parker, and 5) more recently covid (which has slashed retail channels and forced brands to seek sale elsewhere).

In addition, this spring, Facebook announced Facebook Shops, a way for users to seamlessly purchase items from their favorite businesses directly on Facebook and Instagram, which will only serve to dramatically increase the possibilities for DTC. Perhaps one of the most interesting differences between the ecommerce shopping experience in China versus that in the rest of the world is the role of social features in the process. In China, the biggest ecommerce companies are heavily integrated into social media and messaging (e.g. Pinduoduo is built almost entirely on Tencent’s WeChat platform) and strong social elements are married with the purchasing experience (e.g. on Pinduoduo, consumers can see what their friends are buying, join buying groups, and even play games that connect to the purchasing behavior… think Farmville meets Facebook meets Groupon meets Amazon).

With this move by Facebook, a new digitally native Gen Z population, and the blueprint of China’s market, we are likely to see growth in “social-selling” in the US.

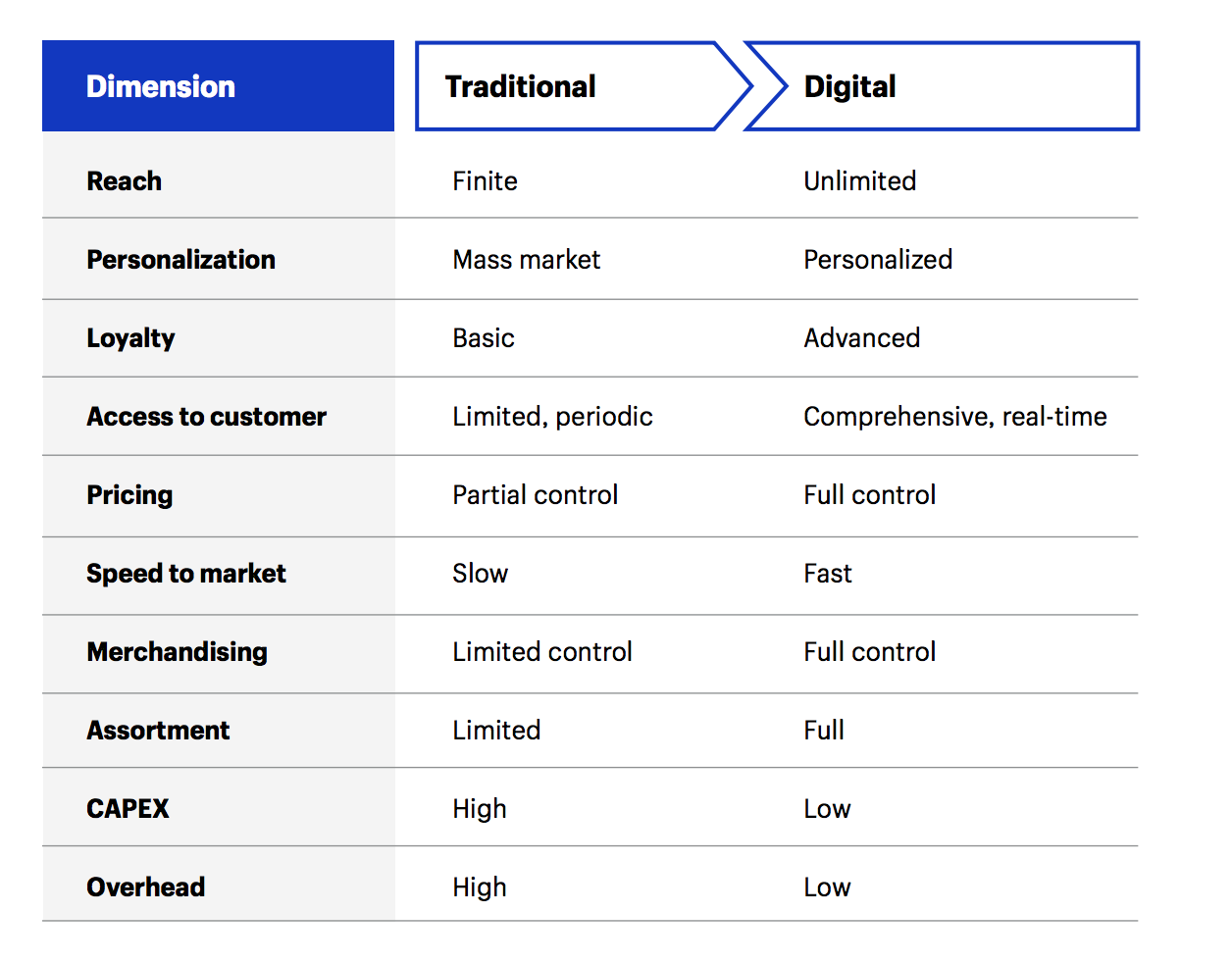

Some of the key areas of opportunity that DTC affords to brands over traditional retail through the direct customer relationship include:

5/ New innovations in shipping, logistics and fulfillment will be a key focus.

With Amazon pushing the envelope and offering standard one day shipping, consumer expectations are heightening and moving closer toward same-day (same-hour?) delivery. Combined with a high return rate, covid, and recent government tariffs, pressure is mounting on supply chains and shipping costs. Amazon’s shipping and fulfillment costs alone totalled $78 billion in 2019 or 28% of their total sales. Innovation here is key to keep costs in check and meet service expectations. Some initiatives companies are taking include 1) structuring incentives to better align customer purchasing behavior to optimized logistics (free shipping thresholds, lower shipping for longer delivery times, etc); 2) multi location inventory warehousing to reduce transportation costs and time; 3) buy online and pick up in store options; 4) technology experiments such as drone delivery (In 2016, the U.S congress legalized the commercial use of unmanned aerial vehicles (UAV) and Amazon launched its Prime Air program in early 2020) and self-driving delivery robots (e.g. Starship technologies); 5) greater connectivity between the systems of retailers and brands to provide visibility over broader inventory and support activities such as “drop shipping”; etc.

6/ Point to point solutions will continue to be developed to enhance key components of operations to “level up” to Amazon.

What has been proven over the years is that very large companies can be built by attacking singular “picks and shovels” problems in large commercial value chains. For example –

“during the gold rush, it wasn’t the miners that made the real money. It was the toolmakers, the workers that manufactured the implements necessary for the droves of miners to strike it rich. We remember Levi Strauss & Co but few rarely can recall top gold miners of the time. The toolmakers made riches; the vast majority of the miners went home empty handed.”

Whether it be Bolt and NS8 for the check out process and fraud detection, Afterpay or Affirm for “buy now, pay later” payment options, ROKT for relevant recommendations at purchase, ShipBob for Amazon level shipping logistics, Happy Returns or Loop Returns for an optimized returns process, Recurly for recurring subscription payments, or otherwise — the size of the market, the ability to market through the marketplaces of shopify and other platforms, and the significant impact that marginal moves of the needle on any ecommerce metric can have, makes the opportunity for point-to-point, “picks and shovels” solutions to be successful.

That said, key players in the space will start to diversify product offerings and leverage customer relationships into new opportunity areas driving some consolidation — for example, Yotpo (which just raised their $75 million Series E) now offers a product suite spanning SMS communication, loyalty programs, reviews and ratings, and visual marketing.

7/ With a recent emphasis on sustainability and ethical commerce, brands will increasingly prioritize the environmental integrity of their products for positioning.

Brand sustainability has been important in recent years, but not critical. But that is beginning to change as it turns out Gen Z and Millennials really care. Companies such as Packhelp are helping to ease brands’ carbon footprint through ecological packaging. Further, DHL GoGreen and DPD Total Zero offer climate neutral shipping solutions to help ease the burden on companies. Brands have begun to innovate different ways to integrate sustainability into their business model whether it be reforming their return policy, repurposing their packaging materials, or sourcing from ethical manufacturing. Online retailers are incorporating sustainability into their mission statements more regularly today.

———————–

We are in exciting times for the space and it will be interesting to see how things pan out. One thing is for certain — the future will be significantly shaped the depth and longevity of covid.